20. Data analysis#

We have seen some elements of data analysis in the previous chapters. For example, we have seen how to extract basic statistics from DataFrames or how to add some regression analysis to plots in seaborn. Here we extend this exploratory analysis and present how true modelling can be performed using SciPy and StatsModels.

SciPy#

Scipy is one of the core packages of the scientific Python ecosystem. It underlies many other domain-specific packages such as as scikit-image (Computer Vision) and implements a large number of complex numerical methods or offers an interface to existing efficient methods (LAPACK, BLAS). Here we only give a few simple examples of the possibilities offered by the package.

Optimization#

Optimization is generally speaking the search for the values of parameters of a function. Typically in data analysis it is used to find the parameters best describing a dataset. Let’s say we have measurements \(y_i\) at positions \(x_i\) and a model \(f(x, a)\), our goal is to minimize the distance between the values \(y_i\) and the predicted values \(y = f(x_i)\), for example by computing \(g(a) = \sum{(f(x_i, a) -y_i)^2}\) and then minimizing \(\min\limits_{a} g(a)\).

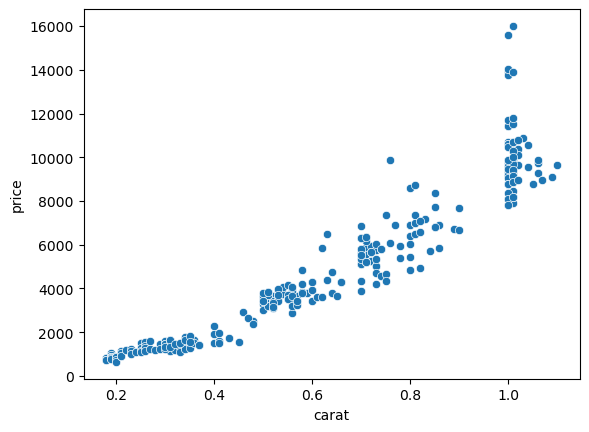

Coming back to our diamonds dataset, we can for example try to create a model for the price vs. carat relation:

import seaborn as sns

import pandas as pd

import numpy as np

import scipy.optimize

diams = pd.read_csv('https://raw.githubusercontent.com/vincentarelbundock/Rdatasets/master/csv/Ecdat/Diamond.csv', index_col=0)

sns.scatterplot(data=diams, x='carat', y='price');

We can define our model as a function. Let’s try a simple line:

def fun_line(x, a, b):

return a * x + b

Now we can directly use the curve_fit function to fit our data. We only need to specify the function, which should take as first parameter the independent variable x and then the fitting parameters, and the actual data \(x_i\), \(y_i\).

fit_params, _ = scipy.optimize.curve_fit(fun_line, diams.carat, diams.price)

fit_params

array([11598.88403958, -2298.35762217])

As output we get the best guess for the fit. The curve_fit can take many additional options for more complex cases. For example you can choose the specific optimization method from an extensive list, specify constraints, initial parameters etc.

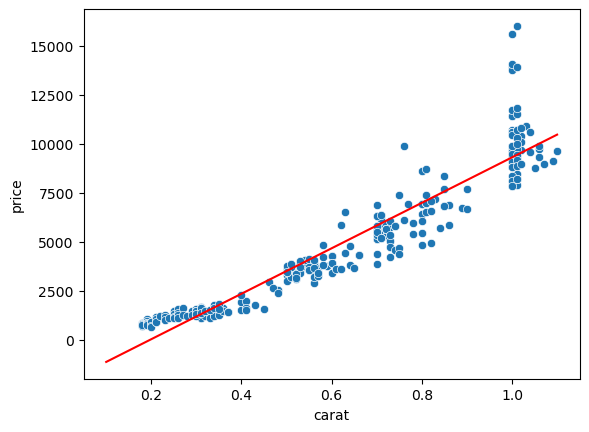

Let’s check the quality of the fit:

ax = sns.scatterplot(data=diams, x='carat', y='price');

ax.plot(np.arange(0.1, 1.2, 0.1), fun_line(np.arange(0.1, 1.2, 0.1), *fit_params), 'r-');

Signal processing#

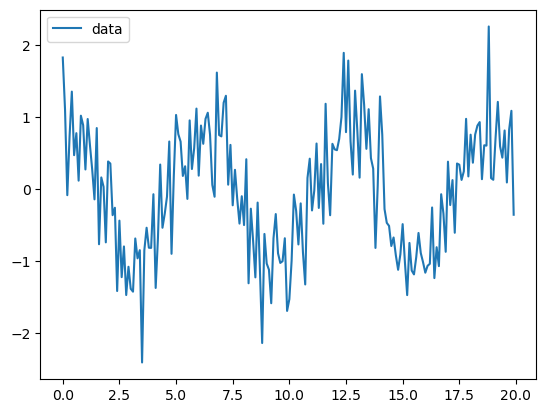

SciPy offers an entire module dedicated to signal processing where you can find a large variety of function for filtering, splines, Fourier transforms etc. For example if you have a signal corrupted by additive noise you can use the Wiener filter out of the box. Let’s create some artificial noisy data:

x_vect = np.arange(0,20,0.1)

y_vect = np.cos(x_vect) + 0.5*np.random.randn(len(x_vect))

sns.lineplot(x=x_vect, y=y_vect, label='data');

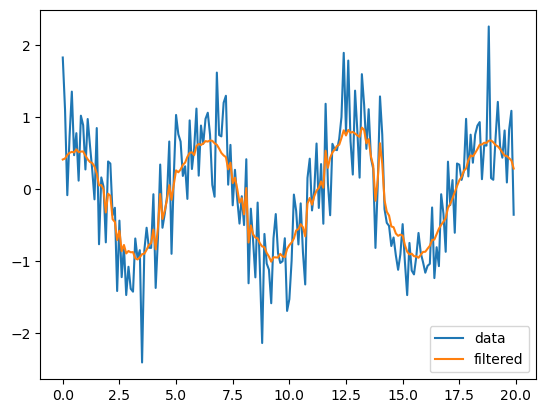

Now we create a filtered version of the data using the Wiener filter:

import scipy.signal

filterd_y = scipy.signal.wiener(y_vect, 20)

ax = sns.lineplot(x=x_vect, y=y_vect, label='data')

sns.lineplot(x=x_vect, y=filterd_y, label='filtered');

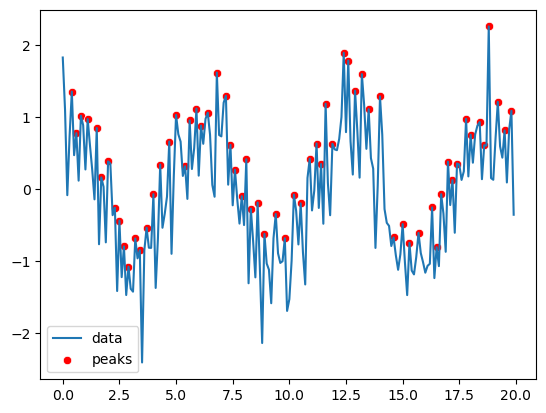

The package contains also useful analysis functions e.g. to find peaks in a signal. For example, let’s try to find peaks in our noisy signal above:

peaks, props = scipy.signal.find_peaks(x=y_vect)

What is returned here is a list of indices where a local maximum was found. We can use that list to plot them:

ax = sns.lineplot(x=x_vect, y=y_vect, label='data')

sns.scatterplot(x=x_vect[peaks], y=y_vect[peaks], label='peaks', color='red');

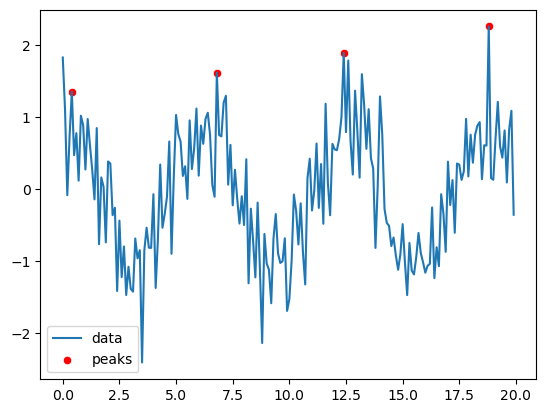

We can then use options proposed in the function to improve the results. For example we can set a window within which to search for local maxima and a minimal height:

peaks, props = scipy.signal.find_peaks(x=y_vect, distance=30, height=0)

ax = sns.lineplot(x=x_vect, y=y_vect, label='data')

sns.scatterplot(x=x_vect[peaks], y=y_vect[peaks], label='peaks', color='red');

statsmodels#

The statsmodels package is entirely dedicated to regression, statistical analysis and test. Of course it partially overlaps with other packages (for example curve fitting in SciPy), but it provides in a simple way standard statistical information not readily available otherwise.

Ordinary Least Squares#

OLS allow one to fit linear models (liner in the coefficients) to datasets and estimate the quality of the fit. For example we can perform the same fit as we did above for the price vs. carat data. First we load the main module:

import statsmodels.api as sm

For our fit, we need now to provide a dependent (price) and an independent variable (carat). Our model does not necessarily reduce to a simple linear model but could have dependencies on multiple variables. All variables can be passed to the fitting model as Pandas DataFrames or Series. For the start let’s just use price and carat in our OLS model:

model = sm.OLS(diams.price, diams.carat)

This returns a model object (similarly to scikit-learn), and now we have to execute the fit:

res = model.fit()

The res object contains all the information about our fit. In particular we can have a look at a summary:

res.summary()

| Dep. Variable: | price | R-squared (uncentered): | 0.943 |

|---|---|---|---|

| Model: | OLS | Adj. R-squared (uncentered): | 0.943 |

| Method: | Least Squares | F-statistic: | 5081. |

| Date: | Tue, 28 Mar 2023 | Prob (F-statistic): | 4.65e-193 |

| Time: | 10:46:27 | Log-Likelihood: | -2678.4 |

| No. Observations: | 308 | AIC: | 5359. |

| Df Residuals: | 307 | BIC: | 5362. |

| Df Model: | 1 | ||

| Covariance Type: | nonrobust |

| coef | std err | t | P>|t| | [0.025 | 0.975] | |

|---|---|---|---|---|---|---|

| carat | 8543.7399 | 119.855 | 71.284 | 0.000 | 8307.899 | 8779.581 |

| Omnibus: | 173.273 | Durbin-Watson: | 0.734 |

|---|---|---|---|

| Prob(Omnibus): | 0.000 | Jarque-Bera (JB): | 1029.681 |

| Skew: | 2.348 | Prob(JB): | 2.56e-224 |

| Kurtosis: | 10.627 | Cond. No. | 1.00 |

Notes:

[1] R² is computed without centering (uncentered) since the model does not contain a constant.

[2] Standard Errors assume that the covariance matrix of the errors is correctly specified.

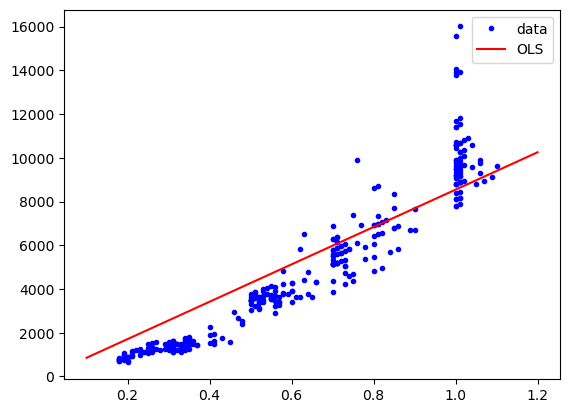

We can alos use the fitting information to generate a plot e.g. by using the predict method:

import matplotlib.pyplot as plt

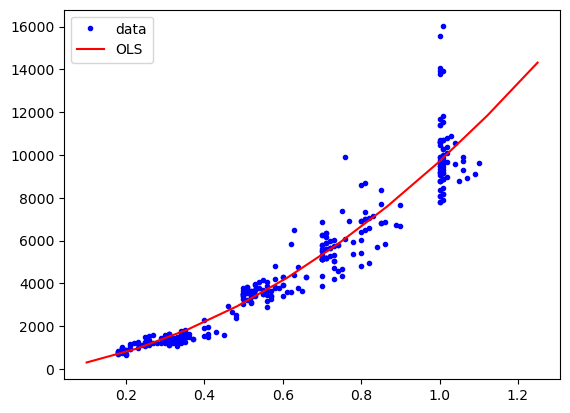

plt.plot(diams.carat, diams.price, "b.", label="data")

plt.plot(np.arange(0.1,1.25,0.1), res.predict(np.arange(0.1,1.25,0.1)), "r-", label="OLS")

plt.legend()

<matplotlib.legend.Legend at 0x15327c790>

We see that our model is too high. The reason for this is that at the moment, our model is simply \(y=a*x\) and thus the intercept is at 0. We can add an intercept to the model by adding a constant column to our independent variables:

indep_var = sm.add_constant(diams.carat, prepend=False)

indep_var.head(5)

| carat | const | |

|---|---|---|

| 1 | 0.30 | 1.0 |

| 2 | 0.30 | 1.0 |

| 3 | 0.30 | 1.0 |

| 4 | 0.30 | 1.0 |

| 5 | 0.31 | 1.0 |

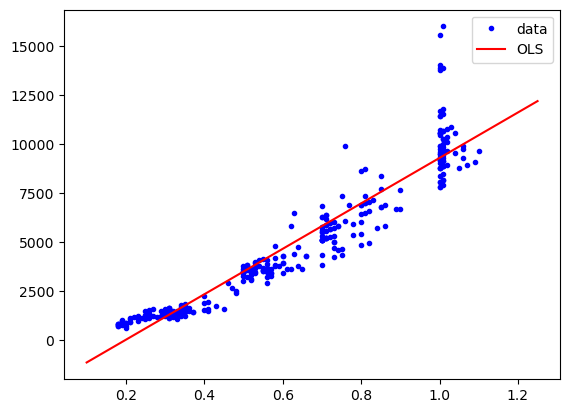

Now we can fit again. Note that for the prediction, we need to create an array (or dataframe) with the correct dimensions, here two columns, one for the carat, the other for the constant.

model = sm.OLS(diams.price, indep_var)

res = model.fit()

plt.plot(diams.carat, diams.price, "b.", label="data")

plt.plot(np.linspace(0.1,1.25,10), res.predict(np.column_stack((np.linspace(0.1,1.25,10), np.ones(10)))), "r-", label="OLS");

plt.legend();

Finally, we can try to use a more complex model. Remember that we have a linear model in the coefficients but we can use a more complex model like \(y = a * x + b * x^2 + c\). For this we add ourselves a quadratic variable in the table:

indep_var['sq'] = diams.carat**2

indep_var.head(5)

| carat | const | sq | |

|---|---|---|---|

| 1 | 0.30 | 1.0 | 0.0900 |

| 2 | 0.30 | 1.0 | 0.0900 |

| 3 | 0.30 | 1.0 | 0.0900 |

| 4 | 0.30 | 1.0 | 0.0900 |

| 5 | 0.31 | 1.0 | 0.0961 |

model = sm.OLS(diams.price, indep_var)

res = model.fit()

plt.plot(diams.carat, diams.price, "b.", label="data")

plt.plot(np.linspace(0.1,1.25,10), res.predict(np.column_stack((np.linspace(0.1,1.25,10), np.ones(10), np.linspace(0.1,1.25,10)**2))), "r-", label="OLS")

plt.legend();

res.summary()

| Dep. Variable: | price | R-squared: | 0.911 |

|---|---|---|---|

| Model: | OLS | Adj. R-squared: | 0.911 |

| Method: | Least Squares | F-statistic: | 1565. |

| Date: | Tue, 28 Mar 2023 | Prob (F-statistic): | 4.29e-161 |

| Time: | 10:46:42 | Log-Likelihood: | -2568.4 |

| No. Observations: | 308 | AIC: | 5143. |

| Df Residuals: | 305 | BIC: | 5154. |

| Df Model: | 2 | ||

| Covariance Type: | nonrobust |

| coef | std err | t | P>|t| | [0.025 | 0.975] | |

|---|---|---|---|---|---|---|

| carat | 2786.0994 | 1119.615 | 2.488 | 0.013 | 582.953 | 4989.246 |

| const | -42.5072 | 316.369 | -0.134 | 0.893 | -665.050 | 580.036 |

| sq | 6961.7059 | 868.825 | 8.013 | 0.000 | 5252.055 | 8671.357 |

| Omnibus: | 178.954 | Durbin-Watson: | 1.443 |

|---|---|---|---|

| Prob(Omnibus): | 0.000 | Jarque-Bera (JB): | 1680.735 |

| Skew: | 2.232 | Prob(JB): | 0.00 |

| Kurtosis: | 13.538 | Cond. No. | 32.4 |

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

With functions#

We can achieve the same results as above by explicitly defining a function using the ols submodule similarly to what you can do in the R world:

from statsmodels.formula.api import ols

res = ols("price ~ carat + I(carat**2)", data=diams).fit()

plt.plot(diams.carat, diams.price, "b.", label="data")

plt.plot(np.linspace(0.1,1.25,10), res.predict(np.column_stack((np.ones(10), np.linspace(0.1,1.25,10), np.linspace(0.1,1.25,10)**2)), transform=False), "r-", label="OLS")

plt.legend();

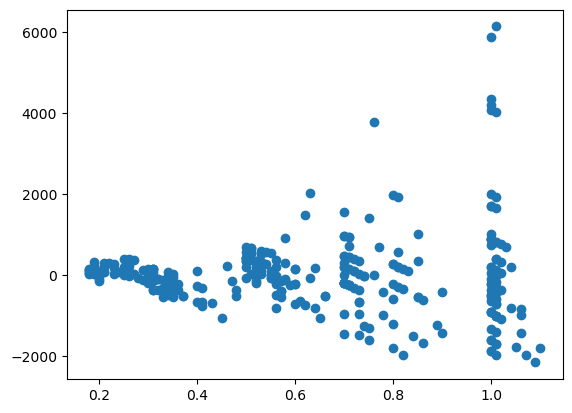

Now that we have a fit, we can check for its quality. For example, we can have a look at the residuals:

plt.plot(diams.carat, res.resid,'o');

The package also offers a stats module that contains a large collection of statistical test. For example we can check whether our residuals are distributed following a normal distribution using the Jarque-Bera test:

import statsmodels.stats.api as sms

test = sms.jarque_bera(res.resid)

test

(1680.7354277013305, 0.0, 2.2315668112919496, 13.537876220126195)

This is just a very short introduction to statstmodels which contains many more models, tools for times series analysis, advanced statistics, tools for plots etc.

Exercise#

Use

scipy.optimize.curve_fitto fit now a parabola (with a \(x^2\) term) to the price vs. carat data. Import the data with:

import pandas as pd

diams = pd.read_csv('https://raw.githubusercontent.com/vincentarelbundock/Rdatasets/master/csv/Ecdat/Diamond.csv', index_col=0)

You are given the noise data below. Try to find the local minima by first without then with filtering the data with a Wiener filter.

x_vect = np.arange(0,20,0.1)

y_vect = 2*x_vect + 3*np.cos(x_vect) + 1*np.random.randn(len(x_vect))

Try to do an ordinary least square fit of the signal knowing there’s a

coscomponent: